Cresting ‘first wave’ of stimulus may be next hurdle for world markets

• Bookmarks: 303

• Bookmarks: 303

LONDON (Reuters) – A growth spurt in the balance sheets of the world’s biggest central banks has crested in recent weeks, drawing warnings from investors that any signs of backpedaling on stimulus will jolt financial markets and strangle economic recovery.

The U.S. Federal Reserve, European Central Bank, Bank of England, and Bank of Japan joined others in March with a wave of stimulus to stem damage from the coronavirus pandemic.

Their combined balance sheets grew by an estimated $5.3 trillion as they expanded quantitative easing programmes via asset purchases, which – hitherto restricted largely to government bonds – now include a wider remit, spanning equities to junk corporate debt.

But as markets have rebounded and economies reopen, that balance sheet surge is levelling off.

Reuters analysis found growth in the four central banks’ balance sheets slowed for the second straight month in June, with some $852 billion added. That was less than half of what was added in April. (Graphic: Cresting wave: central bank balance sheets, here)

“Now that market functioning has largely normalized, central banks are actually reducing their support measures,” BofA rates strategist Ralf Preusser told clients.

Authorities are no longer in fire-fighting mode as they were during the March-April meltdown. Yet, the slowdown is significant.

First, a resurgence of coronavirus infections here worldwide is forcing authorities to reimpose lockdowns, dashing hopes of swift economic recovery.

Second, emergency government schemes, such as worker furloughs and benefits supplements, are also due to expire.

That’s rekindled fears of a “taper tantrum”, similar to the market panic which ensued in 2013 when the Fed hinted at unwinding stimulus.

“The recovery is actually at risk from insufficient fiscal efforts, and central banks will turn more, not less, aggressive,” Preusser added.

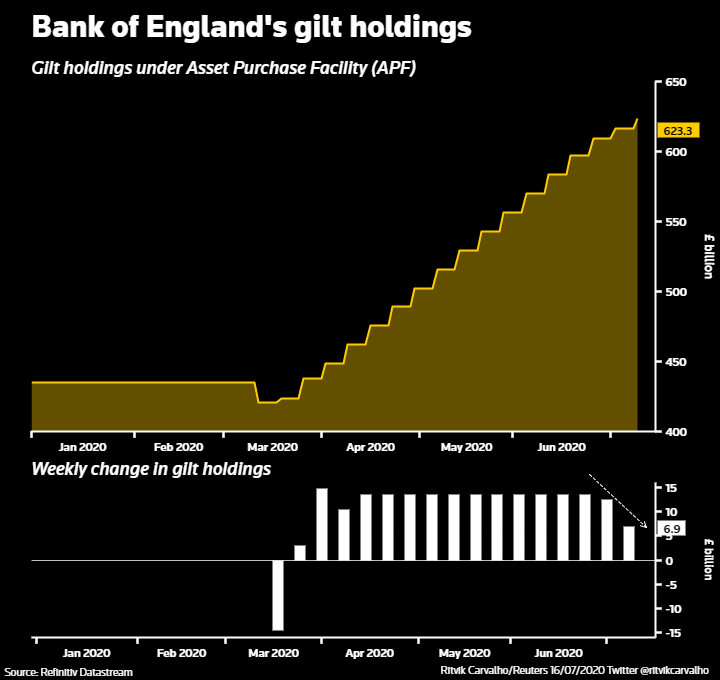

(Graphic: Bank of England’s gilt holdings, here)

WARNING

Evidence of stimulus deceleration is widespread. The BOE has halved its rate of gilt purchases and cited some signs of economic recovery, while the Reserve Bank of Australia has not purchased any assets since early-May.

The BOJ this week effectively suggested a pause in monetary easing.

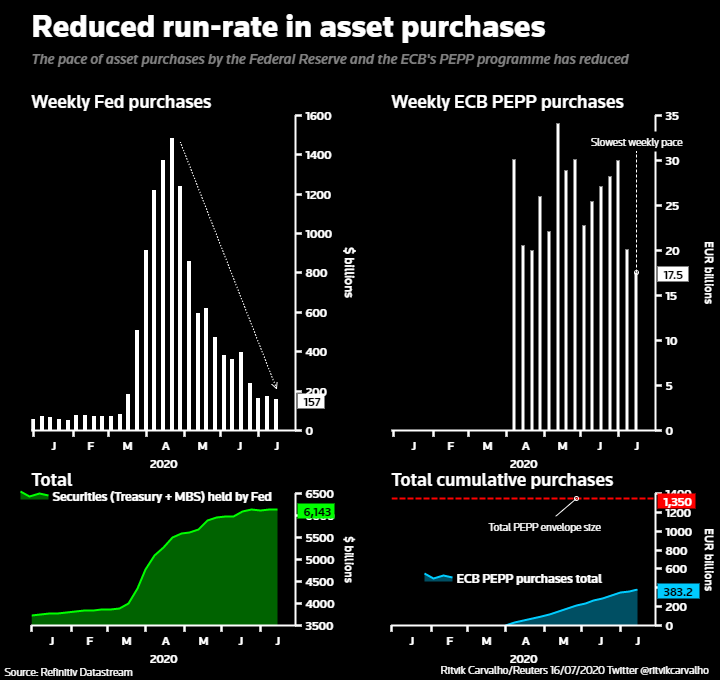

And at the ECB, weekly bond purchases under the Pandemic Emergency Purchase Programme (PEPP) fell to 17.5 billion euros last week, the slowest since its start in March.

Danske Bank chief strategist Piet Haines Christiansen estimates the ECB is buying at a rate of about 4 billion euros a day. At that pace, he reckons the ECB could hit the PEPP’s 1.35 trillion-euro limit by next June.

But various ECB policymakers have indicated that limit may not be fully utilized. That would mean a substantial decline in purchases, Christiansen says.

“Markets do not appreciate that yet,” he warned. “Markets expect full PEPP implementation so if purchases are scaled back well below the 4 billion euros a day, we may see a reaction in markets.”

It’s not all bad news – bond markets were reassured on Thursday by ECB President Christine Lagarde who said the PEPP facility would be fully utilised.

Meanwhile, the Fed balance sheet shrinkage is mostly down to reduced demand for its swap and repo facilities as global dollar shortages eased.

(Graphic: Reduced run-rate in asset purchases, here)

“BENEFITS CLIFF”

The looming expiry of U.S. and European worker support schemes, however, remains a concern, said Jim Leaviss here, head of fixed income at M&G Investments.

“The second half (of 2020) will be all about the new taper tantrum,” Leaviss added.

First up is the end-July expiration of a $600 weekly supplement for unemployed Americans — dubbed the “benefits cliff” by Deutsche Bank, which sees this as one of the defining moments for markets this summer.

Asset manager BlackRock cited that cliff as a reason to cut U.S. equities here in favour of Europe, where a ground-breaking recovery fund is under debate to aid hardest-hit states.

But worker furloughs start winding down across Europe too this autumn, including in Britain, Spain and Netherlands.

IMF Managing Director Kristalina Georgieva warned here on Wednesday it was premature to start withdrawing safety nets, while Lagarde said the cliff needed monitoring.

Ultimately though the prospect of market tantrums may be what deters authorities from hitting the brakes too hard.

Daniel White, senior research and strategy manager at Canada Life Investments, said the sheer scale of stimulus meant some tapering was inevitable, but authorities would tread carefully.

“The story of the past 15 years is that governments and central banks have become hostages (of markets),” White said.

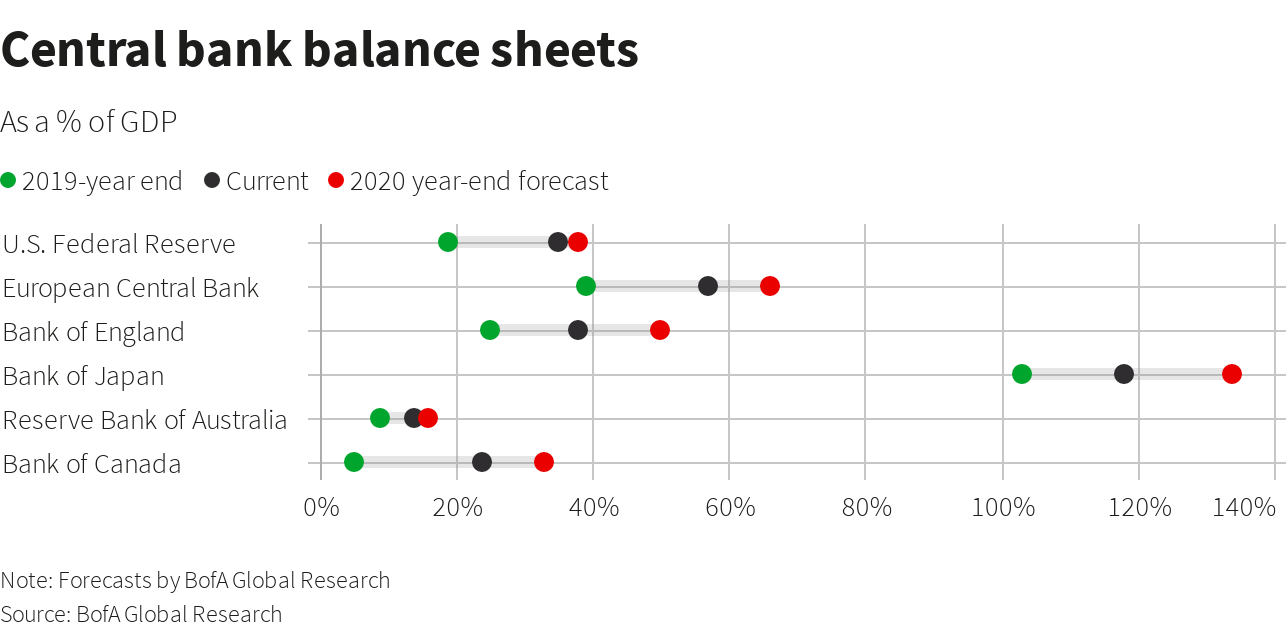

BofA predicts balance sheet expansion to resume too- its analysis shows every major central bank will end 2020 with a bigger balance sheet than now.

For interactive graphic here (Graphic: Central bank balance sheets Central bank balance sheets, here)

0 comments

0 comments Share

Share

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}